Midwest Startups during COVID-19: CEO Survey Results

Not all doom + gloom

Following our recent survey on Midwest VC activity during COVID-19, Sandalphon Capital conducted a survey of Midwest Startup CEOs to gauge the impact COVID-19 has been having on their companies. There is some fear and uncertainty in the tech sector on both investor and startup sides, and we thought we could shine a light on the current status of a typically opaque sector.

The results will cover the following areas, and include some commentary based on our six years experience investing at the Pre-Seed to Series A stages in startups across the Midwest:

- General Impact

- Revenue Impact

- Headcount + Compensation Impact

- Fundraising Impact

If you would like to review the full survey results please download the PDF here.

A huge thank you to everyone that took the time to complete this anonymous, relatively lengthy survey, or passed it along to CEOs. Responses are from a fairly representative mix of 197 Midwestern Startup CEOs between April 24 and May 5:

- Startups with headcounts of up to 250 employees (mean of 16) and that have received up to $80 million of funding (mean of $5 million) accounting for over 3,000 jobs and almost $1 billion of invested capital.

- We did not ask about specific areas of focus or verticals to help maintain anonymity.

Two major caveats to bear in mind:

- All responses are specific to the nuances of any given business model, end market, team, company maturity, and fundraising situation which may differ greatly.

- Any inherent bias around who is and is not predisposed to respond to a survey like this given their current situation.

If you want to hear about future surveys, results, other research and content, please sign up for our email list here, or follow Sandalphon Capital on Twitter.

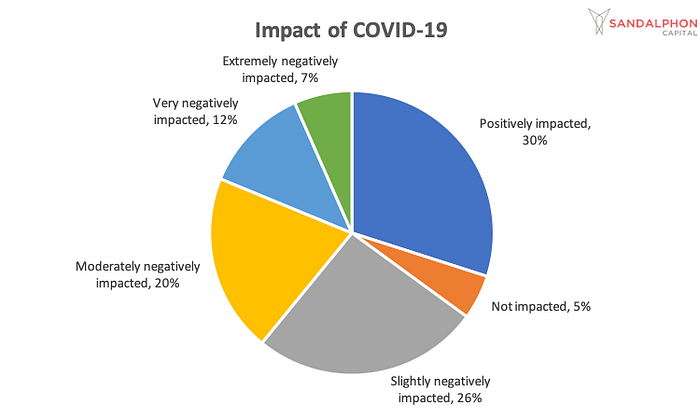

1. General Impact

Over 60% of the startups surveyed have been positively-to-slightly negatively impacted by COVID-19, and only 19% very or extremely negatively impacted.

Of the 59 startups positively impacted, 49% of these report that their revenue has increased, 19% report flat revenue, and 19% are pre-revenue. Fifty-six percent of companies report that their pipeline or revenue outlook for the rest of this year has increased, 14% see no change to their 2020 outlook, and 10% see a 0–20% reduction in expected revenue this year. The median runway of the positive cohort is twelve months.

Of the 19% very or extremely negatively impacted, 22% of these are pre-revenue and half have seen revenue declines of 40% or more. Their median runway is six months.

Forty-five percent of B2C respondents and 30% of B2B respondents have been positively impacted. Enterprise B2B has fared better than SMB-focused. MedTech and B2B selling to SMBs have been the most negatively impacted: 47% and 60% of them were moderately to extremely negatively impacted, respectively.

Sentiment

Two thirds of startup CEOs reported being a little-to-very optimistic despite this challenging environment. Optimism versus worry generally maps to the extent of revenue increase or decline. Optimists (a little-to-very optimistic) are expecting quicker recovery: on average 4 months quicker than those that are a little-to-very worried.

As one CEO noted: ”Investors seem scared. Founders don’t.”

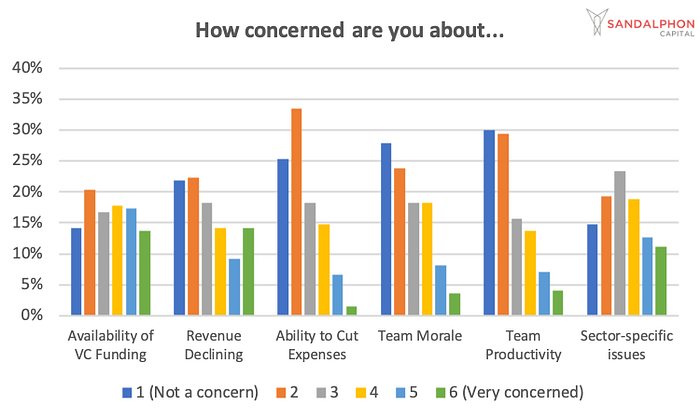

The availability of VC funding is not yet as big a concern as expected. Within the 51% of respondents reporting low concern (1–3), median runway is 12 months (16% of them are profitable). The high concern group has only 8.5 months of runway. As you might expect, VC funding is not a concern for bootstrappers (9% of respondents) and was a low concern for 70% of the 20 Series B stage respondents. The vast majority of responses varied based on their particular circumstances.

Likewise, revenue declines and sector-specific issues are idiosyncratic to any particular startup’s business model or area of focus, but in general the concern scores were relatively moderate, likely due to the temporary nature of these headwinds in most cases.

The vast majority of startups appear to have adapted to working from home given team productivity and morale is holding up well. Additionally, the ability to cut expenses does not appear to be a problem. Approximately three-quarters of CEOs scored these factors a low concern.

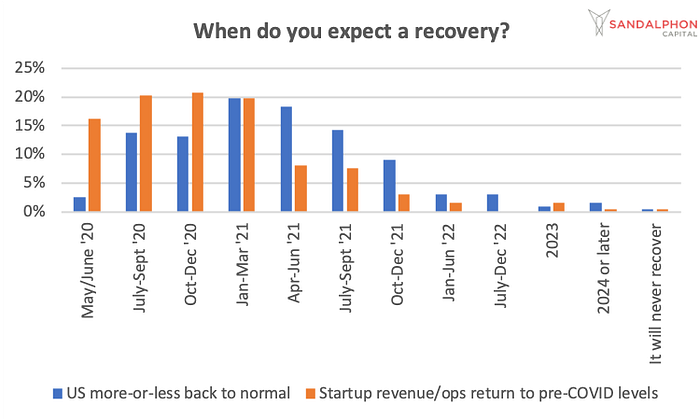

Recovery Expectations

Respondents expect an average of four more quarters until a recovery. Twenty-nine percent of CEOs expect the US to return “more-or-less back to normal” during 2020, 61% during 2021, and 6% in 2022.

Fifty-seven percent expect startup revenue or operations to return to pre-COVID levels this year; 39% during 2021. On average there is an expectation that startups will recover approximately one quarter prior to the US overall.

A recovery will take longer than expected as we are still early in a recessionary cycle, even as stay-at-home orders are eased. It will take take time for the economy and confidence to heal: recessions usually continue for at least four quarters. Startups will need to be planning accordingly, and investors will need to be exceptionally forward-looking.

On average, the CEOs indicated that their recovery estimates depend on a few conditions. Lifting of stay-at-home orders, availability of widespread testing, and certain sectors reopening are the most commonly cited factors. Over a third do see a vaccine as being important to meet their recovery expectations.

Other conditions provided include a general return of economic confidence, unfreezing of purchasing decision-making processes, successful executions of pivots, and some sector-specific issues like schools reopening or hospitals returning to offering full services.

Seventy-two percent expect a 75–100% chance of survival if conditions persist (or worsen) for 3–6 months. Almost a third put their chances at worse than a coin-toss.

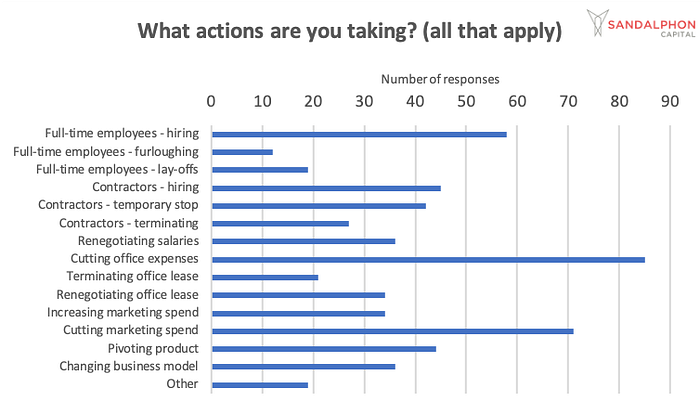

Actions Taken

Given the impact of COVID-19 and current expectations, many CEOs are cutting office-related expenses and marketing spend, but also still hiring in many cases. Other changes cited include adding lower price tiers, renegotiating contracts, expanding to other verticals, reducing founder salary, shifting but not cutting marketing spend, adding unpaid positions, and trying to establish remote hiring methods and processes.

Seventy-three percent of respondents are somewhat-to-very supportive of stay-at-home orders, more than four times those that are somewhat-to-very unsupportive. There is no clear pattern as to how supportive these CEOs are based on any other factor in the survey, suggesting that in general they are not letting their own personal circumstances dictate their view on these orders too much.

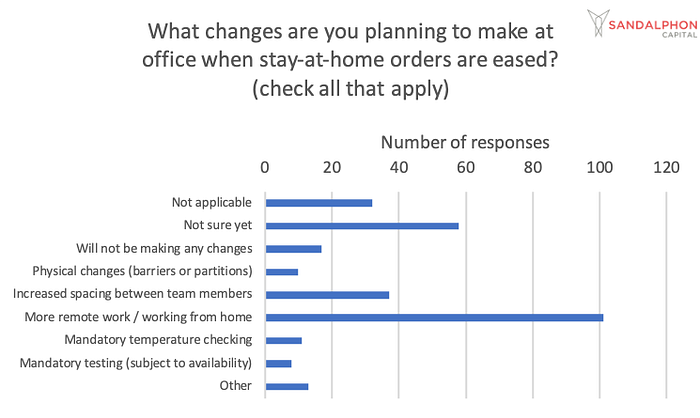

When the stay-at-home orders are eased it seems that remote work is here to stay in many cases (half of respondents). We failed to include “providing or requiring PPE” as options, but one CEO noted that it would be required when interacting with the public, and another for in-person meetings. Almost a third are “not sure yet” so the sector will need more information on official guidance or requirements.

Here are the shelved guidelines from the CDC for re-opening workplaces (see last page). Truss, an office leasing startup and Sandalphon portfolio company is providing some relevant resources on their website to help understand what to do with office leases and layouts during this time.

Of the 126 respondents that were VC-backed, 62% have found their investors to be helpful, primarily with board-level support and strategic advice, as well as support for current fundraising efforts or loan applications. Eighty-three percent of startup CEOs have found their investors have been able to spend enough time with them. Those in the other 17% should make sure they explicitly let their investors know they need more support.

2. Revenue Impact

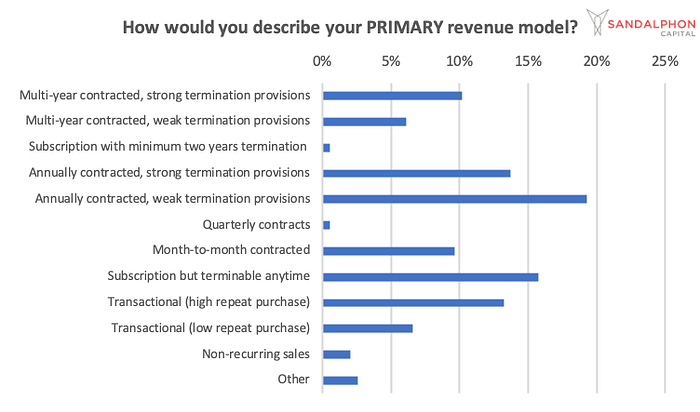

To put this section in context, survey participants reflect a range of different business models. The intent is not to suggest any particular revenue model is more or less superior or appropriate, only to highlight the differences.

Nineteen percent of startups post-revenue with multi-year contracts and strong termination provisions have seen revenue declines, but none down more than 40%; 73% of those with multi-year contracts and weak termination provisions have seen declines, with nearly half down 40% or more. Those with annually contracted revenues performed the same regardless of termination provisions, with half of them seeing declines.

Sixty-three percent of those post-revenue with month-to-month contracts saw declines, but none down 40% or more. However, 59% of those with subscriptions terminable any time saw declines, with over a third of them down 40% or more. This difference may indicate a lesson about the importance of creating some friction around cancellations.

The outlook for the rest of this year is very mixed based on the idiosyncrasies of any given startup.

Side note on growth + fundraising

Investors like to invest in growth, and growth is currently very hard to achieve in many cases. For many, their investable universe may have shrunk. Additionally, investors in the current climate may have to throw out most of their usual screening criteria and take a longer term view. Year-over-year or month-over-month revenue growth, LTV:CAC, “SaaS Magic Number,” conversion rates… All of these signals have gone haywire, and it will take months to build enough datapoints to prove out key metrics again. In many cases, investors do not have a pressing need to put money to work in the coming months, and their bar has never been higher.

Startups that need to fundraise are going to need show signs of capital efficient growth, in whatever form they can. If funding is required to finish building a product, try pre-selling with mockups, form some co-development relationships and/or build a waitlist. Early customers might prepay or invest in the startup themselves. To buy time while pilots to convert, get as many pilots as possible to make conversion risk less binary: more “shots on goal,” more pilot customers that can be interviewed to gauge product-market fit. For those that need to hire sales people, consider experimenting with commission-only for now. Try and get the middle-to-late stage of the sales pipeline looking as fat as possible to create some near-term visibility to revenue. Absent observable revenue growth, founders must do whatever they can to look like a coiled spring, ready to rapidly expand on the other side of this.

Investors will have to squint a little to have any visibility into growth or momentum. They will need to think more than usual about what the business looks like 2-3 years out instead of 6-12 months out — founders should make that as obvious as they can for them. Investors will have to have confidence in what they have seen working before in terms of value propositions and go-to-market playbooks. They are, after all, investing in where the startups will be in 3-10 years, not 6-12 months.

“Be fearful when others are greedy, and greedy when others are fearful.”

- Warren Buffet

3. Headcount + Compensation Impact

Despite the headlines about job losses that typically relate to larger startups, 78% of respondents have not yet made any reductions in headcount. For those retained, just over half of the CEOs have been able to maintain full pay for everyone so far, but this varies greatly by the particular circumstances of a startup or its team.

For those that have made cuts they have been deep, with a mean reduction of 9 FTEs or 60% of their headcount. The median reduction is only 3 FTEs given our survey is skewed towards smaller, early stage companies. One third of startups have implemented a hiring freeze for 2020, another third continues to hire but at a slower pace.

Clearly CEOs are doing what it takes to get through this. Around half have already reduced their own compensation with others indicating in the comments that they will be doing so soon. As you might expect, this generally corresponds to revenue impact and length of runway.

4. Fundraising Impact

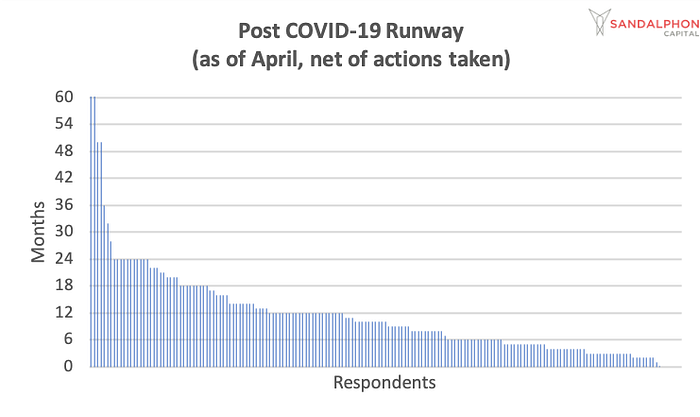

The vast majority of startups are burning cash with varying degrees of near-term funding needs. With the impact of COVID and after actions taken to decrease burn, median runway across the startups as of April was 10 months (mean of 11). Thirty-six percent have a runway of under 6 months, and another 27% 6-12 months.

Median runway pre-COVID, as of February, was reported to be 12 months (mean of 13) so, with two months passing as of April, runway would also be 10-11 months excluding any impact or actions taken. This suggests that in the aggregate, the impact of COVID and actions taken have netted themselves out.

Twenty-three percent saw their runway shrink despite actions taken, 19% have not seen a change. Thirty-four percent were able to add 1-3 months, 11% added 4-6 months, 10% 7-12 months and 4% over 12 months.

We would consider having at least 12 months of runway to be prudent right now unless a business is still growing in the face of these headwinds. It is easier to shorten your runway later than to extend it.

Fundraising Plans + Experience

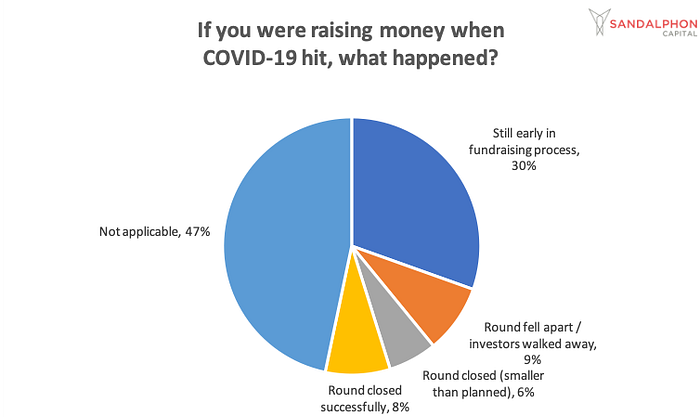

Forty percent of CEOs have delayed their fundraise, either out of necessity due to investor appetite, or because of runway extension. Twenty-nine percent are fundraising right now, 10% are not going to be fundraising. For everyone else the median length of time until they plan to start fundraising is six months. This suggests startups are allowing four months to raise money, given a current median runway of ten months.

We would recommend starting a fundraise earlier and allowing longer for the fundraising process. It will take longer than normal for investors to build conviction, and if everyone hopes to start their fundraise when conditions improve then bandwidth of investors will again be an issue. Investors can only dig in on so many opportunities at the same time. Start to build relationships, get feedback, refine your narrative. Start to give investors “dots” of progress that they can extrapolate into a “line” of execution and momentum as soon as you can.

Fundraising in the last few months has been a mixed experience. For those who did not raise the amount they were hoping for, hopefully they are continuing a dialogue with investors, and can continue to show progress. Regular updates go a long way at the moment. Check out our recent survey of Midwestern VC investors to better understand what they are currently thinking.

Government Support

Payroll Protection Program (PPP) and Economic Impact Disaster Loans (EIDL) are the primary additional sources of funding specific to small businesses for this crisis. Ineligibility is around the same for both at ~18-19%. The PPP loans are much more popular than EIDL loans, with only 7% eligible but not interested in PPP versus 30% for EIDL, presumably given the forgiveness of the PPP loans.

Of those that have applied for a PPP loan only 53% have received funds, and only 20% for EIDL. These funds are needed more urgently for some than others, but this certainly highlights some of the issues that startups have encountered with these programs. More external financial support is going to be needed in many cases to keep these small businesses alive.

It has been interesting to see the varying degrees of government support of this ecosystem across the Midwest. For example, Michigan quickly launched a Tech Stabilization Fund whilst other states or cities have done nothing. If you are aware of any specific initiatives in your region please let us know or make a note in the comments below. We need a supportive environment where the jobs and employers of the future are protected, risk taking is encouraged, and unnecessary financial losses are minimized, or we risk setting back the Midwest tech ecosystem many years.

5. Conclusions

The long-term outlook for our region remains positive. It is worth noting that our sample compares very favorably with a study done by Startup Genome that found that 74% of startups globally have trimmed staff (versus 22% in our survey) and 65% have less than six months runway (versus 36% in our survey). We seem better positioned than many to weather the storm thanks to Midwestern capital efficiency and pragmatism.

The impact of COVID-19 has varied greatly, but the sentiment is optimistic. If you have been hit hard by this, you are not alone. If you have seen tailwinds from this, hopefully you can really appreciate how fortunate you are. Investors are generally being helpful but will need to figure out how to take a long-term view without strong near-term signals. CEOs are generally doing what it takes, and the survey suggests there is room for further action in many cases where necessary. For those that have been laid off, or where startups do not survive this, there are still plenty of tech companies expanding across the region where your skills and experience can make a huge difference.

If you would like to review the full survey results please download the PDF here.

Nearly all respondents expressed interest in participating in another survey in coming months as conditions evolve, so if you want to make sure you hear about future surveys and results please sign up for our email list here, follow Sandalphon Capital on Twitter or hit “Follow” on Medium. If you have any suggestions on how we can improve this survey next time please leave a comment below or send us a quick note here.

Office Hours: If you are a founder of a Midwest startup that is not yet VC-backed, and would be interested in office hours to get some feedback ahead of your fundraise, please complete this form.

Suggestion Box: What else would you like us to write about?

Jonathan Ellis is the Founder and Managing Director of Sandalphon Capital, a Pre-Seed to Series A stage VC firm established in 2016, based in Chicago and focused primarily on the Midwest. He was previously a Senior Vice President at Macquarie where he spent ten years making private equity and debt investments in middle market companies and special situations. He holds a BSc (Hons) International Management from the University of Manchester and a Masters in Finance from INSEAD.

Sandalphon’s Midwestern portfolio companies include Avail, Balto, Backstitch, Chowly, Daupler, Jiobit, Kin Insurance, LogicGate, MyCOI, Page Vault, Provi, Quevos, RealVision, Regroup Telehealth, The Minte, Structurely, Supernova, TripScout, Truss and Vertex. At the time of writing Sandalphon is between funds and is not actively investing in new opportunities.