Survey results: Midwest VC activity during COVID-19

As the Managing Director of Sandalphon Capital, a Chicago-based, Midwest-focused, early stage VC firm, I was recently asked to share my thoughts on how startups can try and survive COVID-19.

I pointed out that “many institutional VCs and angels are pausing new investments and the bar will be high for those with dry powder to deploy.” I thought now would be a good time to try and understand how bad conditions really are, and to check the pulse and sentiment of the Midwest VC ecosystem: What are fundraising prospects like right now?

Last week I sent a survey to 106 VC firms, angel groups and family offices across the Midwest and received 68 responses. For context, these are primarily “early stage” perspectives, with 56% of respondents indicating they invest in Pre-Seed rounds, 84% Seed, 69% Series A, and only 11% Series B or later.

The first question was, “How would you describe the current status of your firm?”

Only 28% of firms are currently operating “business as usual.” The vast majority (47 respondents, or 69%) are focused on their current portfolio. Happily, most of these (37) are still taking meetings with intent to invest near-term, however ten are only taking “early meetings” for now. VCs have a responsibility to their portfolio company founders, teams and own investors (LPs) to help their current investments navigate these challenging times, but the results suggest an appetite to invest is still there for 82% of them.

So, many are still interested in investing — but how hard is it going to be to get a meeting?

Almost two-thirds are being “a little more selective” to “much more selective.” To some extent this is due to competing demands on time e.g. working through current portfolio issues, or the challenges of working from home such as juggling work with childcare. This is also partly driven by the desire to filter for startups that seem to be able to survive or thrive in the current climate (more on this below).

The more boards a VC sits on, the larger their portfolio, or the more “hands-on” they are in their investment approach, the less bandwidth they may currently have. If you are a founder that is raising and they say “no” to a meeting, make sure you ask for feedback on “why” so you can adjust your approach accordingly, if necessary.

When do they expect to be comfortable be investing again?

Almost half are comfortable investing right now and several firms have confirmed they are actively making new investments. However, for many, their estimate on timing depends on one or more factors, as illustrated by the select feedback below.

34% say their investment timing is not being affected by COVID-19:

“Agnostic. Better to invest in a great company now than later.”

“Crisis hasn’t affected our comfort in making new investments, just slowed pacing.”

“We invest very early, so this hasn’t changed our thesis re: long term value creation.”

“The right deal at terms that feel appropriate.”

24% say it depends on how the startup is doing, or will do, in a

“post-COVID world” and another 4% need to see adequate runway to get past this crisis:

“18–24 months runway in conservative scenario/even stronger and more experienced team/industries that are expected to thrive during and post COVID.”

“Certain industries are minimally effected by this crisis, they are the most likely candidates for new investment.”

“Assessment of viability and growth as the pandemic and lockdowns persist into 2021 and beyond.”

19% would like more clarity on when the economy will start to reopen and recover, and 4% are looking for their portfolio to stabilize so they have more bandwidth:

“More certainty around when economy will “re-open.”

“Testing and a national plan/road to reopening of the economy.”

“Better understanding of the economic impact of the virus.”

“Want to see some economic data on the impacts of the crisis. May want to see if the second wave comes in the fall.”

“We’re giving the economy a chance to settle. Would like to see macro indicators turn positive.”

6% cite “working from home” issues e.g. they can’t meet team in-person

“Need to be able to meet people in-person.”

“Just getting comfortable making investments without meeting founders in-person and getting to know them better.”

Overall, 43% expect their number of new investments in 2020 to be “a little lower,” 7% “much lower,” 34% “flat”, and 16% “a little higher.”

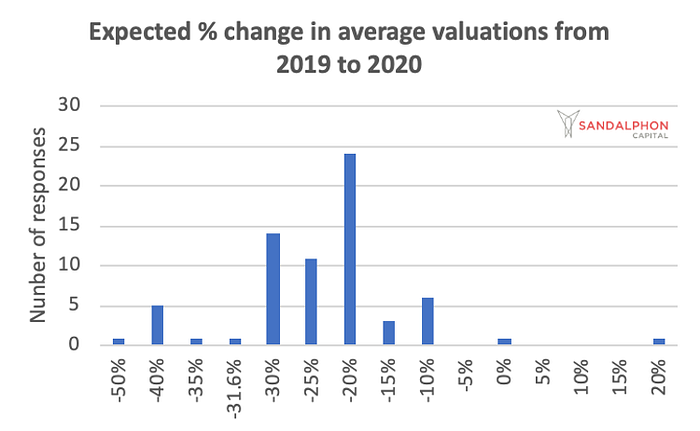

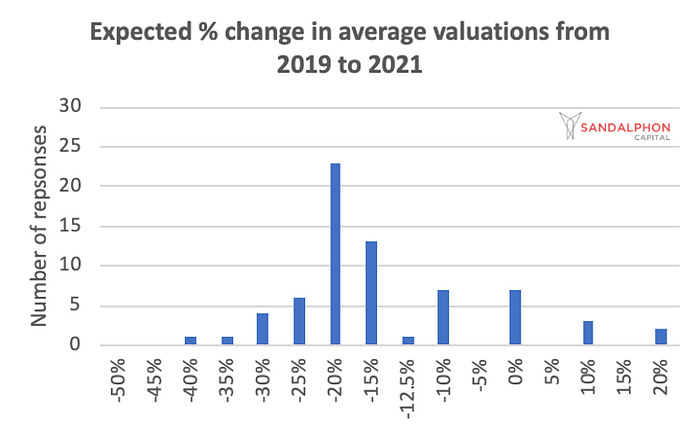

How is the COVID-19 crisis impacting valuation expectations for the near future?

Most respondents are expecting a 20–30% average valuation decline in 2020 versus 2019 (mean of -23%) with a slight recovery to a 15% decline in 2021. However, this will certainly vary based on idiosyncracies, and how strong the pitch and business model are in current market conditions:

“Different industries will see wildly different impacts. I suspect no change/positive change (higher valuations, faster rounds, etc) in areas like telehealth, collaboration software, etc… versus significant down rounds, challenges fundraising in the sharing economy, travel/tourism, etc.”

Valuation declines are likely in many cases. Some investors point to the decline in the stock market as a direct explanation of this, which I personally disagree with, however:

- Increased macroeconomic risk or uncertainty justifies a higher required rate of return. This translates to a lower valuation entry point, all else equal.

- Valuations reflect growth potential. While it is easier to talk about multiples based on ARR or trailing revenue, it is more accurate to consider valuations on a forward-looking basis. For example, a SaaS startup that raises at 20x ARR may really raising be at 10x expected ARR a year from now. When revenue growth slows down or declines, valuation multiples collapse, and you will need to emphasize the longer-term upside story.

- VCs invest in growth. They like their dollars to be invested in sales and marketing (which increases revenue) and/or product development (which translates into new or stickier customers, higher revenue per customer, more defensibility). This usually results in a meaningful return on invested capital and an increase in valuation. In the current environment a good return on newly invested capital is much harder to achieve.

- If your valuation is likely to go sideways for 12–18 months due to a combination of lower revenue trajectory or valuation multiple compression, VCs will feel like they are better off waiting to invest. You will need to convince them of responsible cash management and an ability to still provide upside, either through a lower-than-hoped valuation today or ability to execute through this crisis. Be scrappy, be resourceful, be creative.

What kind of financing rounds are investors looking to invest in right now?

There is strong preference for “clean”/“up rounds” (or at least “flat” rounds), which in the context of all other responses and market conditions suggests firms are going to be very selective. Current market conditions are likely to create more flat rounds or “down rounds” in otherwise strong companies.

A down round (where money is raised at a lower valuation than the prior round) suggests a startup has not been able to meet its milestones or the company is not faring well in the current environment. “Recaps” are often adversarial due to ownership being re-negotiated or reset, so in a relatively small, collaborative ecosystem these can strain relationships. Investors often prefer to avoid startups that become “storied.”

These are unprecedented times, so I am hopeful that there will be less stigma around such rounds, as they may be necessary to save otherwise good companies. There could be a number of attractive “stressed” opportunities for investors to pursue.

How should you be structuring your fundraise?

There is a universal preference for priced/preferred equity rounds. SAFEs are considered to be “founder-friendly,” but using these will make fundraising from VCs harder than it needs to be right now. Most institutional VCs will not invest in them even in good times given the weak governance and control provisions (however Sandalphon has done so in the past). To maximize your chances of a successful raise, look to do a priced round, or a convertible note, unless you are raising exclusively from angel investors.

So what does all this mean?

There are clearly trends emerging in this climate that you must take into consideration based on your specific fact pattern, but thanks to the growth in the Midwest VC ecosystem in recent years, there are plenty of funding sources with dry powder to put to work for the right startups, at the right price.

Your ability to raise VC funding near-term is going to be heavily driven by how viable your business model and go-to-market strategy currently is, as well as how well you demonstrate capital efficiency and an ability to grow during the current market conditions.

When communicating with VCs, try and understand their bandwidth, realistic timing, and the conditions required for them to invest, so you can manage your burn and fundraising process appropriately.

Recessions have historically been a great time to launch startups, but be careful assuming that this will be over quickly when planning your capital needs. There is not yet a clear path to normalcy.

The one thing I know for certain, is that no-one knows anything for certain.

Thank you to everyone who took the time to complete this survey. If you found this helpful please sign up for our email list here, hit “Follow” on Medium, and follow me on Twitter for more on venture capital, startups and the Midwest ecosystem.

If you have any suggestions on how we can improve this survey next time please leave a comment below or send us a quick note here.

Suggestion Box: What else would you like us to write about?

Interested in additional perspectives?

Semil Shah (GP at Haystack & Venture Partner at Lightspeed) did a quick survey of (coastal) Series A VCs that you can read on Twitter here.

Early into the crisis (March 12th) Tomas Tunguz of Redpoint compared this crisis to the 2008 Global Financial Crisis when deal volumes stayed around the same level but with lower valuations and smaller round sizes. Personally, I think this this time is different — I suspect the breadth of the economic impact and the disruption of stay-at-home orders is going to reduce deal volumes, and sadly some business models are not going to be considered “fundable” until this is over — but this is another good reference point.

Survey respondents:

- Total number: 68

- Responses reflect submissions from April 15th to 19th 2020.

- 58 VC funds, 4 family offices, 3 corporate VCs, 2 angel groups, and 1 angel group/VC fund hybrid.

- 25 in IL, 8 in WI, 7 in MI, 5 in MN, 5 in OH, 3 in MO, 2 in IN, 1 in IA, 1 in KY, 2 in NE, plus a few others/undisclosed.

- 41 “early stage” (Pre-Seed to Series A), 15 “mid stage” (Seed to Post-A), 12 “later stage” (investing through Series B or beyond).

- End-market investment preferences: 63 B2B, 47 B2B2C, 40 B2C, 20 GovTech, 3 Consumer-only specialists.

- Business model preferences: 63 SaaS, 43 Tech-enabled Services, 39 Marketplaces, 24 Hardware/IoT, 16 Consumer Goods / CPG, 19 MedTech (pharma/biotech/med devices).